Bumble Buyout Rumors

So rumor yesterday, Bumble is looking for a buyout. The company undeniably cheap:

They’re making $280M a year on $930M revenue are priced at only 445M. That’s a multiple of 1.5x, or 2.6x if you include their 300M debt (net of cash). Probably one of the cheapest stocks on the market.

I had already been looking at Bumble with a fly’s enthusiasm for rotting meat. There are lots of problems that we’ll get into, but at $2.94 there are 3 reasons to buy:

Reuters announced today Bumble is looking to get acquired. If they get acquired at a very cheap multiple of 5x on 250M Ebitda, that’s $6.60 a share.

Bumble is telling us they’ve stopped bleeding users, maybe, and third party data confirms it. If true Bumble is probably worth maybe $10/share.

Bumble knows they suck. They announced they’re getting rid of the swipe and are pivoting to AI-based matchmaking, with a huge marketing push in Q4. Maybe this is a bad thing, I dunno, but if they succeed this could be worth like $10-$20.

Anyways, there’s at least 3 scenarios in which this is a multibagger. Bumble could also keep dying and go to $0, we’ll see. Let’s start with why Bumble sucks and nobody wants it.

Bumble Origins

I watched the Bumble movie for research, so take this with a grain of salt.

According to the movie Whitney Herd was a cofounder at Tinder. Tinder was apparently a toxic place, she ends up falling out with the cofounders and suing for sexual harassment and wins a settlement. Feeling snubbed, she pairs up with Andrey Andreev, the Russian billionaire cofounder of Badoo, which had taken off everywhere but in the US. Andrey bankrolls Whitney’s founding of Bumble, which was marketed as a woman-friendly dating app.

It worked, kinda, for a couple reasons. First, women on Tinder felt a bit like they were being thrown to piranhas. There’s always been more men than women on dating apps, so women just get bombarded with messages and sometimes unsolicited dick picks, etc. Bumble’s solution was to make the women message first when they match, which isn’t really the natural dynamic but it solved the message spam problem. Bumble establishes itself as #2 in the dating app market behind Tinder, marketing itself as the woman-friendly Tinder alternative.

In 2019 Andrey Andreev, the Badoo cofounder and 79% owner of Bumble, also has a sexual harassment scandal. Not a great look. He gets kicked out and his ownership stake is sold to private equity, BlackStone.

2019-2024: Private Equity Enshittification

BlackStone borrows $3B to buy Andrey’s 79% ownership of Bumble, saddles that debt onto the company and then ipo’s to dump their shares on the public. Along the way they extract as much money as they can. First they fund buybacks when Bumble was trading at $50 a share. Basically transferring all of Bumble’s cash to themselves while they selling shares.

Then they just kinda operated the company in an extremely greedy manner for years without making things better for users. First off, let’s point out that at its core Bumble (and Tinder) use dark patterns to keep users hooked. They know which users are matches, but instead of showing them upfront they stagger out a couple a day, turning the app into a slot machine. On the transcripts they said they had developed better algorithms, but they kept it as a paid feature. Meanwhile their focus was on rolling out “consumables”, fake flowers guys can pay to send women, etc. Their only real attempt at innovation was a weird blockchain pivot they considered in 2022. Zero focus on actually getting users better dates.

“we have dozens, if not hundreds of experiments going on at any given time”, “price optimization and pricing analytics and price testing… is core to the DNA of Bumble”, “our goal is always to maximize revenue in any market.” etc.

So by 2023 an analyst straight up asked them on the call “are you sacrificing the health of the product in order to drive revenue growth.”

2024: Bumble Removes The One Thing That Made Them Unique

So first, Bumble’s ads in 2024 are out of touch, some women really did not like this:

Bumble’s main distinguishing feature was making women message first. This wasn’t necessarily a great feature, but it was Bumble’s identity, their motto was “make the first move”. So around 2022 Bumble decided, hey wait we can monetize this, and added compliments, essentially men can message first but only if they pay! Yikes.

Then in 2024 some men’s rights activists sued Bumble saying their policy was discriminatory. So Bumble relaxes the one thing that made them unique, and lets men message first. Their internal metrics improved, but they destroyed the only thing that made them stand out from other dating apps. They became a Tinder with less users. Meanwhile, Match Group (Tinder owner) comes out with Hinge, which is basically Bumble with slightly less dark patterns. Users start leaving:

2024-Now: Bumble comes to Jesus

Whitney Herd and other execs step down. The new CEO admits the obvious, they have focused entirely on monetizing their users without investing in their product. “Quality reset” is the term. Ad spend is cut 85%, a third of the employees are laid off.

They actually made some decent changes. They started requiring verified ids to cut out bots and spammers. They remove some ways they were monetizing users, start talking about making the free experience better.

After a year, Whitney Herd comes back, speaking a new language. AI-powered Bumble 2.0, powered by a completely new tech backend.

“We are getting rid of the swipe”

“Everyone is exhausted from this passive model of just low-effort likes, low-effort interest with very little follow-through. Frankly, the industry at large—and us included—has made it too easy to express low-intent interest. We are turning that on its head.”

“We are a dating app. We are not a matching app or a swiping app, but have we really been behaving like that?”

A lot of talk is currently being talked. The official narrative from Bumble is that the 5% quarterly decline in users was on purpose as part of a quality reset, and “the kpis have stabilized in Q2”.

“the interaction model is outdated, not just for us, but for the industry at large. I believe it is time to leapfrog anything that currently exists.” “I really believe that this is going to be category-defining, and we want to keep it close to the chest.”

“we expect to introduce the initial features of our new interaction model and profile. This is our big bang. It will start to roll out to select markets in Q4, backed by a 360 marketing campaign.“

Is Bumble Dying?

So where does this leave us...as we’ve seen, this company is kinda shit.

I’m skeptical. Fortunately, none of that needs to be true for this to be a good trade. At 440M market cap for a company making 250M+ a year, the bar is on the floor. If they can slow user decline to like, 3-5% a year (from 5% a quarter!), they could probably be bought out at like $6.30 a share (5x multiple on 250M EBITDA - 300 net debt). If they actually stop declining and start growing again even 2-3% a year, very possible for them to get a 10x multiple and be valued at $15 a share.

So how fast is Bumble dying? They are claiming their user decline was intentional, which nobody believes, but they have a point that kicking users out and cutting marketing 85% has had an impact. They are claiming that “kpis are stabilizing” heading into Q2.

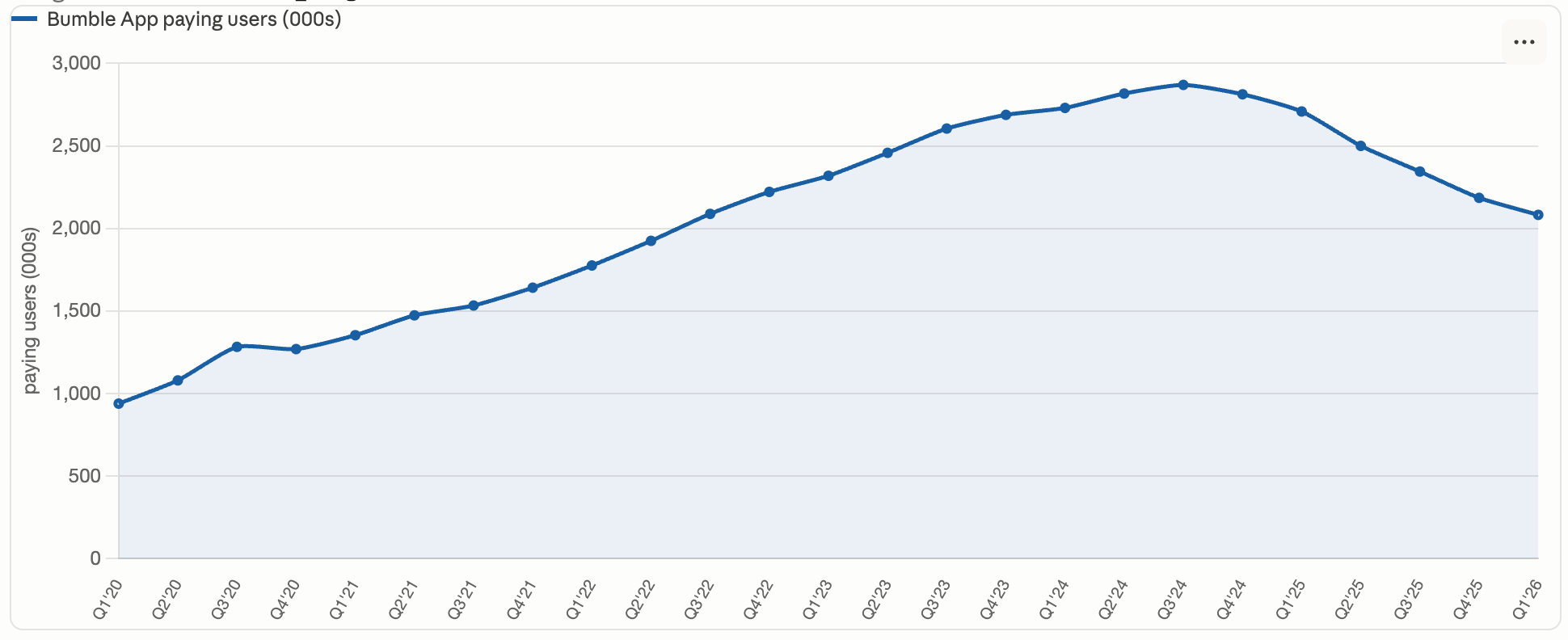

We’re kind of seeing a flattening on the user curve:

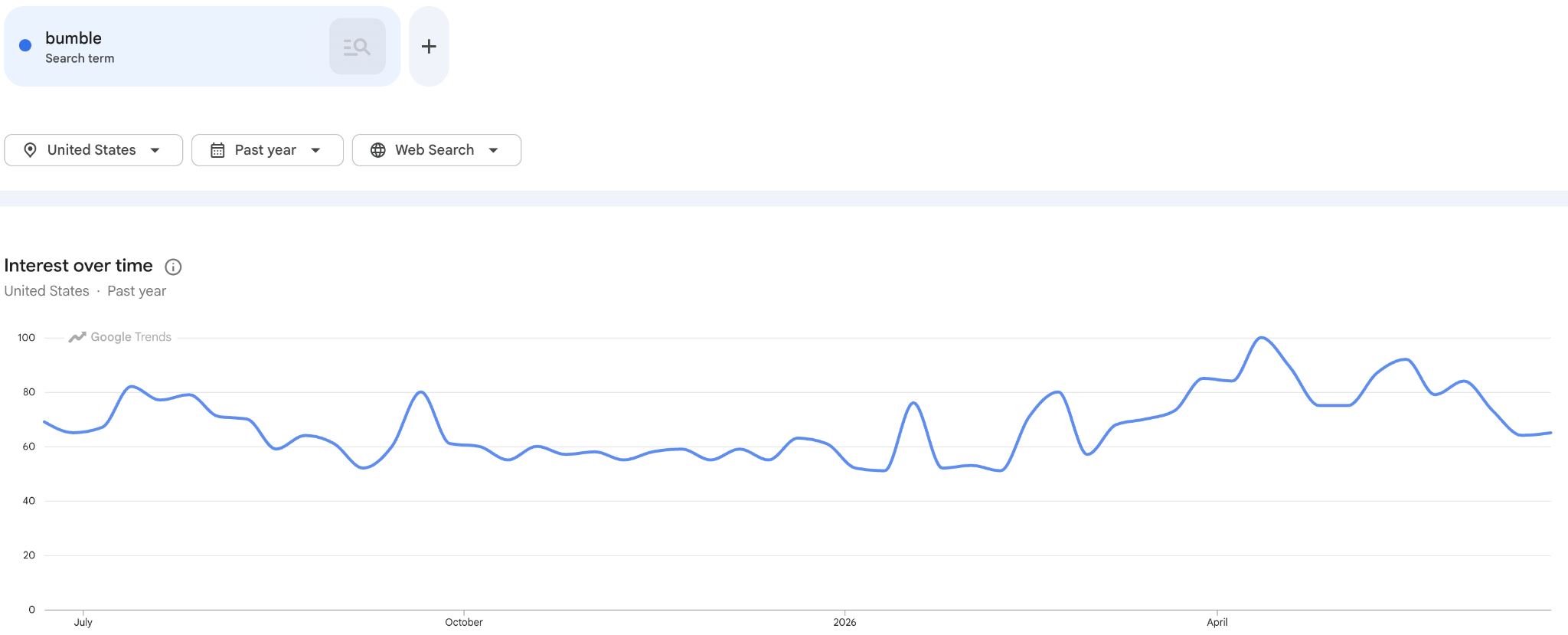

From Google trends it’s not obvious Bumble is dying, if anything it’s had an uptick:

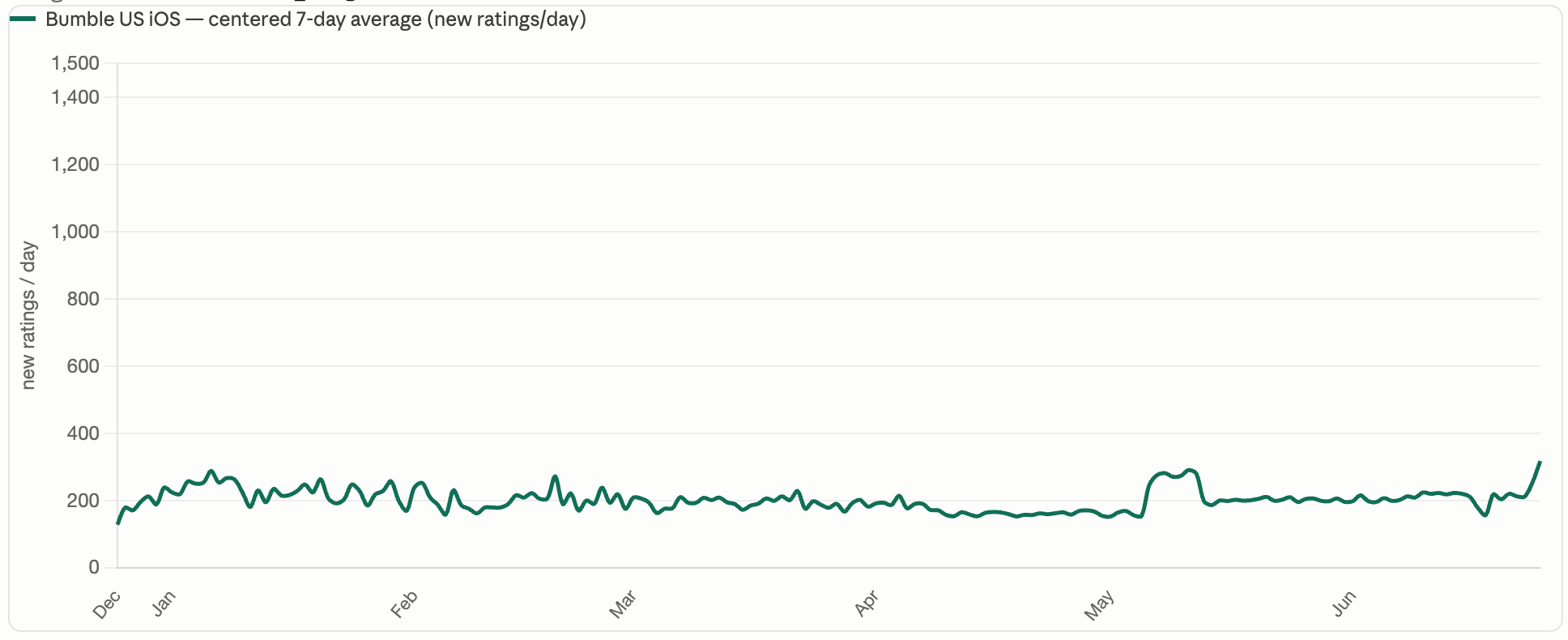

I got a trial to a site that collects app data (AppTweak), here’s the number of daily iOS ratings for Bumble in the US:

You can see the drop from January through May but in the last two months it has inflected and is trending up. So we’re seeing early signs that user decline has stalled and is maybe growing again. To reiterate, the market usually values profitable stable companies at multiples like 10x, which in Bumble’s case would be about $15 a share. We’re going to have to see at next earnings on Aug. 5, but if they say users only declined 3% and we project slight growth next quarter, the market could react very positively.

Trade Thoughts

The market isn’t wrong to price Bumble cheaply. Users, especially gen z, are abandoning dating apps. The company’s future rests in an AI pivot that has potential but is unproven. This is a decent set-up for a 6 month trade though. In the next 6 months there are 3 catalysts: a return to slight growth after a year of decline, a potential buyout, and the Q4 launch of Bumble 2.0. All of these have potential to rerate Bumble to $5-$10. The 6-month downside should be limited by their strong cash flow, in the next 6 months they’re going to make $100M+ and continue paying down debt. If none of these things happen by January though I’m out.