$AUNA, WalMart, Sasspocalypse

Auna is a premium Latin American healthcare provider. They own Clinica Delgado, a world-class hospital in Peru that is the preferred choice of Lima’s elite. Auna’s base is in Peru but they have expanded into Colombia and Mexico, with ambitions to cover all of Spanish-speaking Latin America.

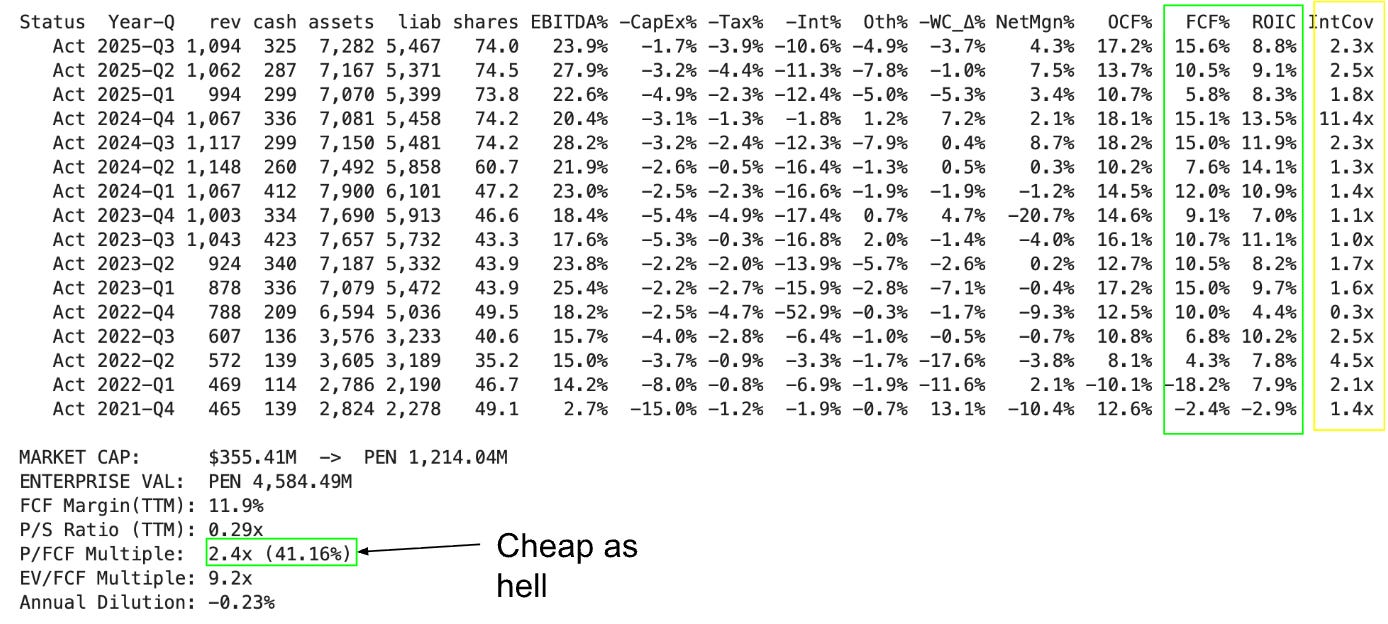

Auna has been growing at 23% a year and are projecting continued growth of 10-14% next year. They’re still growing 11% a year in Peru and just entered Mexico, so growth could continue for a decade or more. They are a combined insurance + healthcare provider, which gives them very good margins for a healthcare company. Medical loss ratio for their oncology insurance (the percent of insurance premiums they have to eat as costs) is 48%, compared to 85-90% for US insurance companies. Check out the financials:

Look at the price / free cash flow ratio of 2.4x. This is a $355M USD market cap company that made about $140M in cash flow in 2025. A normal hospital multiple would be 10-12x. This is a health provider with elite margins (48% MLR, 10-15% free cash flow margin), projected to grow 10-14% next year, trading like it’s going bankrupt. So why is the market scared?

First, obviously, it’s in Colombia and Mexico. Auna is always going to trade lower than US companies due to geopolitical risk.

Second, debt. Auna borrowed a ton of debt to build hospitals and grow. Debt/Ebitda is at 3.6x, which is high but manageable. The debt situation is improving. Their bonds were recently rated B+ (not junk!). Auna just refinanced their debt at a lower rate and got the IFC to participate in the raise, which was 3x oversubscribed. The goal for 2026 is to reduce debt load down from 3.6x Ebitda to 3.0x. While the debt is being paid down, Auna is bringing on partners to finance their expansion. The Peruvian government is helping them finance a 23-story facility in Lima, and a Japanese conglomerate named Sojitz is co-investing $500M to expand Auna’s hospital network in Mexico.

Third, Mexico. Mexico is Auna’s most recent market. They couldn’t convert the doctors there to the “Auna Way” so they cleaned house and fired the leadership and a bunch of doctors, and the doctors took their patients with them. Between that and some IT/billing issues, Mexican revenue dropped 12% in Q3. Auna insists this is part of the process but the market clearly was spooked.

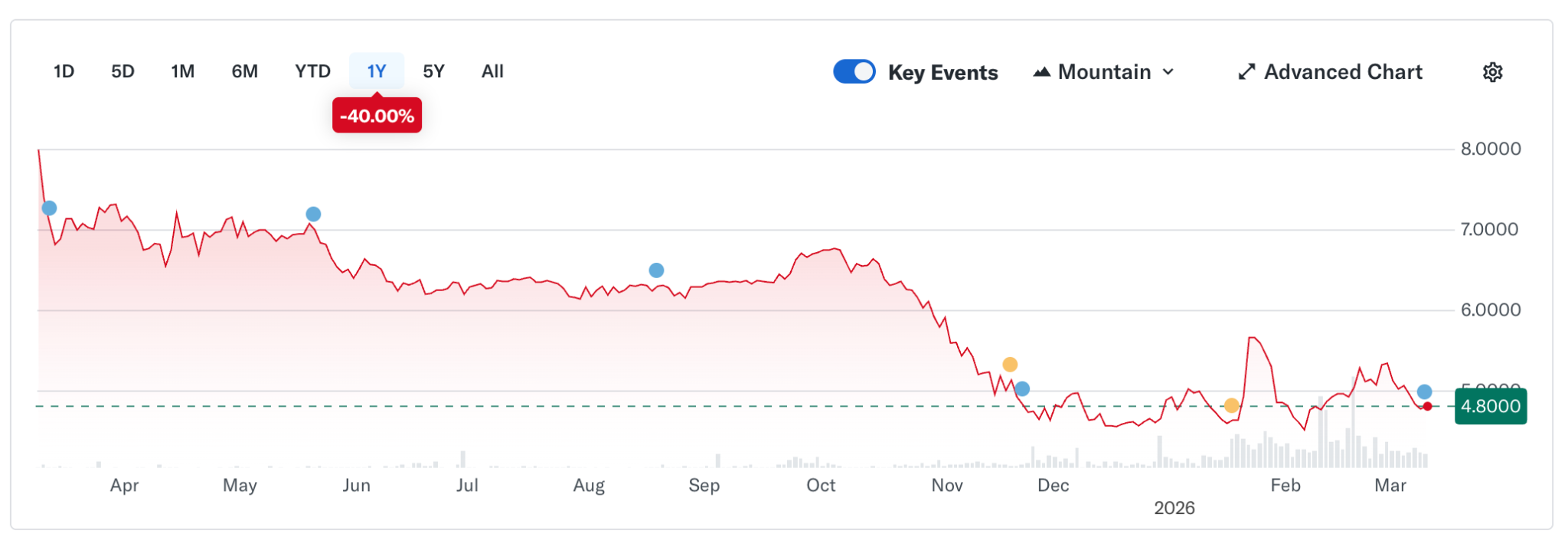

Finally, Grupo Ángeles. They were making an acquisition attempt on Auna and got blocked by Mexican regulators, and decided to dump 15% of the total shares onto the market, ending in February. You can see it clearly:

Q4 earnings just came out today, and the biggest fears holding this stock back are being lifted. Mexico has recovered from -12% revenue growth in Q3 to only 3% in Q4, with 35% growth in high margin oncology and cardiology divisions. Management is projecting 10-14% overall Ebitda growth for next year and targeting reduction in debt from 3.6x to 3.0. Free cash flow for 2025 is up 35% compared to 2024.

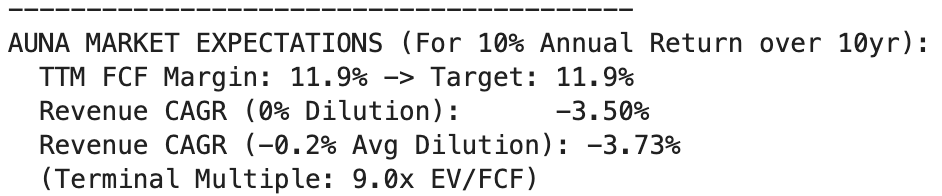

Anyways, the stock is up 15% after hours on the good news, which should bring the price / fcf multiple from 2.5x to 2.8x. Still not a lot priced in, if we believe the discounted cash flow models, Auna could shrink 3% a year and still give an annual 10% return for a decade:

I’m thinking this could be a great 2 year hold. Jeffries had a $9 target and Morgan Stanley $10 before the quarter so the after hours price of $5.60 isn’t expensive yet. If Auna continues to grow 10-15% a year and pay their debt down to a comfortable 2.5x debt / Ebitda ratio, we should see a 10-12x multiple on $180-$200M USD free cash flow, which would put it at $20-$25 a share, a 4-5x from here.

US Market is Expensive

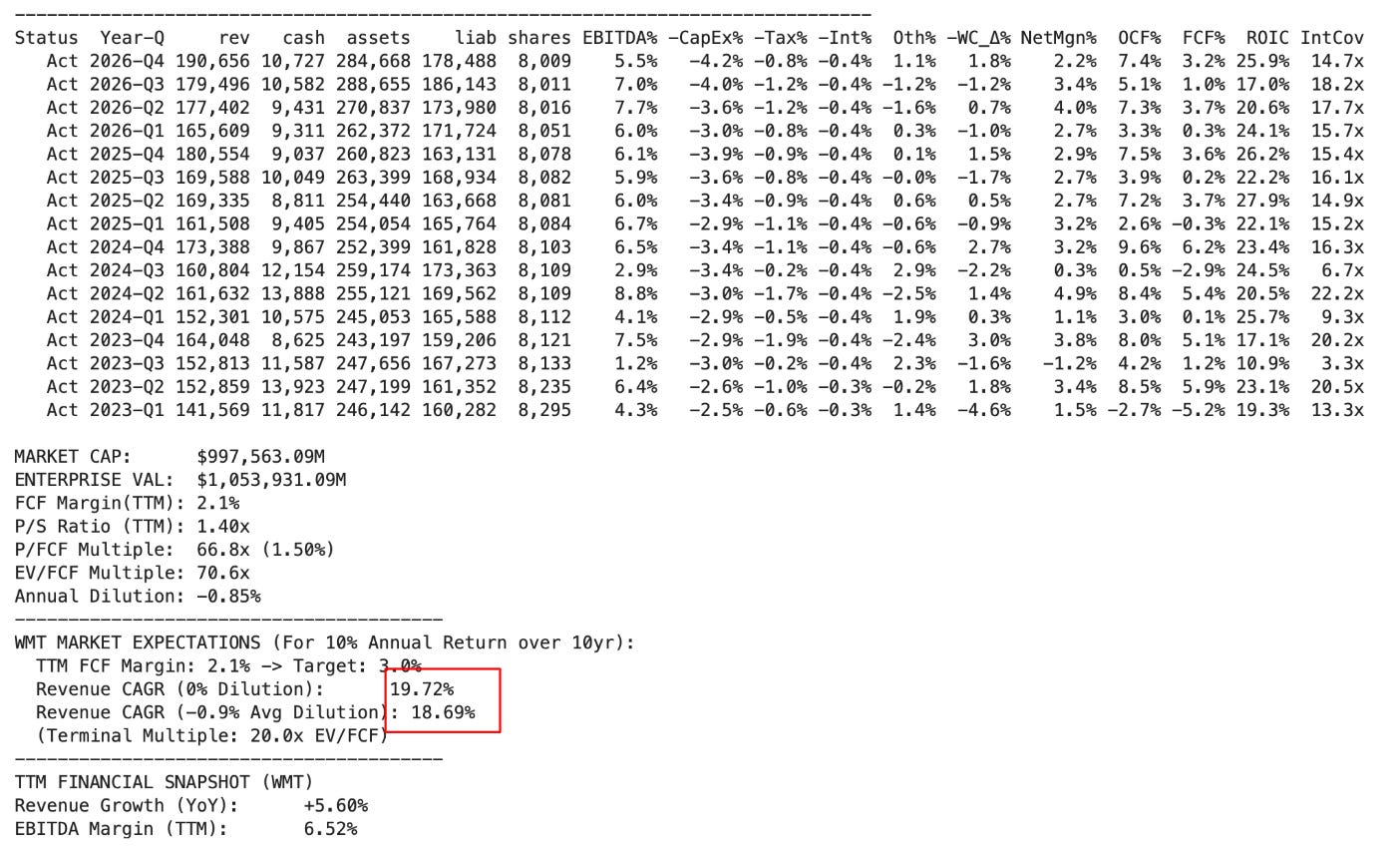

Stock prices in the US are getting stupid. Look at WalMart:

WalMart is trading at a P/FCF of 67. That’s a tech company multiple. WalMart is a slow-growing company that has had 2-3% margins for decades. At this price it needs to grow 18% a year for the market cap to make sense.

WalMart isn’t the only one, most well-known US companies have double-digit revenue growth already priced in. $TSLA has 50% annual growth priced in. With these expectations, chances are the US market is in for a lousy decade. I’ve started looking internationally to diversify. I switched over to Interactive Brokers (shameless referral link) because Fidelity was charging me 1% for international trades. I’m finding some decent deals in Europe, and will try to post some once I’m done hunting.

Sasspocalypse

Yesterday’s cool tech stocks are now unfashionable and cheap:

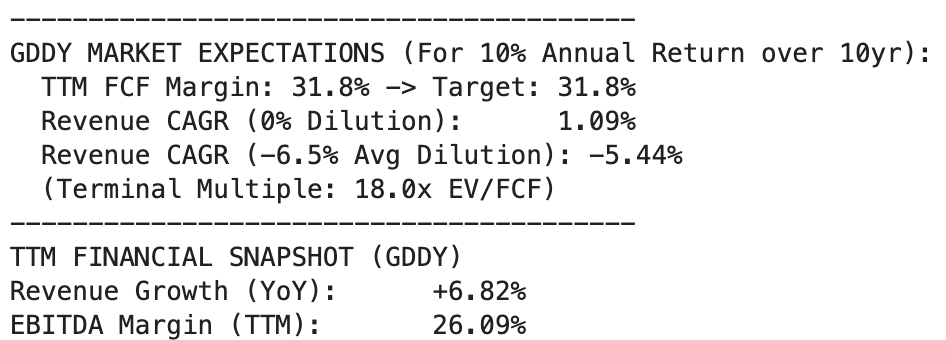

Godaddy ($GDDY) is at a P/FCF of 8x and buying back shares. It’s a high-margin business with strong brand awareness, and at the rate it’s buying back shares its revenue can shrink by 5% a year and still return 10% annually to shareholders. They’re projecting 6% growth.

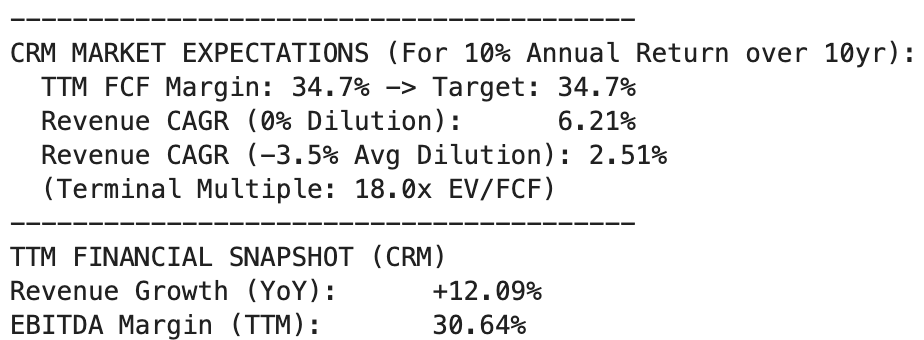

Salesforce ($CRM) is at 13x FCF and has a $50B buyback. They just announced they’re going to borrow $25B just to buy back shares faster. At current prices they just have to tread water and buy back shares to give a 10% annual return to shareholders. They’re projecting 12% growth for 2026.

For both stocks we can get roughly a 10% return if they just don’t shrink. If they hit their growth targets that rises to 20%, and if they get rerated back to tech stock multiples it could be 50% or higher. Worth considering at these prices.